What is Know Your Customer (KYC)?

What is a KYC (Know Your Customer)?

KYC is an abbreviated form of know your customer. Know your customer is a systematic process that business enterprises carry out in order to verify the identity of their respective potential customers. Know Your Customer regulations aid businesses to identify customers with criminal intentions and protecting their business from illicit financial transactions. Nowadays, entities of all sizes have Know Your Customer procedures in place to ensure that their potential customers, consultants, representatives, or distributors are genuine and bonafide.

Read more about: The importance of Customer Identity Verification

Insurers, banks, and many other financial institutions, and the Designated Non-Financial Businesses and Professions (DNFBPs) are rapidly employing detailed customer due diligence (CDD) processes. Know Your Customer or KYC plays an essential role in determining and eliminating the risks associated with serious crimes like money laundering, corruption, bribery, fraud, terrorist financing, and other illicit financial activities.

What is the importance of Know Your Customer (KYC)?

Know Your Customer or KYC is a standard global requirement within the economy, specifically for the industries with huge investments and high-risk elements. It is a process from the regulatory bodies of the industry in order to protect all the stakeholders within the industry. Therefore, KYC is in the best interest of any investor or investment firm, especially when a considerable amount of money is at stake.

In addition to the Know Your Customer process for new customers, conducting KYC for existing customers or investors is also required. Maintaining accurate and updated records in the organization about clients is critical.

Here is the importance of KYC for business organizations as well as customers.

What is KYC in Banking?

KYC is the short form for Know Your Customer. KYC in Banking is the process of identifying and verifying customer identity while opening a bank account and during the course of business.

The purpose of KYC in the banking industry is to identify the customer and prevent financial crimes, including money laundering and fraud.

KYC requirements For business organizations/corporates

Know Your Customer process also helps in establishing trust in a professional relationship and gives insights into the nature of the customer’s activities. In addition to that, the KYC process is a crucial part of the customer or client onboarding process. As a result, it can exponentially improve investors’ overall servicing and management over the course of the relationship.

KYC requirements for customers

The need and importance of knowing your customer (KYC) are not entirely clear from the customer’s point of view. Customers often ask why is KYC required? However, the protection of the economy from financial crimes is the priority of regulators. All of these rigorous checks can be a cumbersome process for investors. However, they create a trustworthy and secure environment to enable investment or financial activities with the respective business entity.

Ever-evolving technology allows for a smoother and streamlined onboarding process that helps the customer save a lot of money and, most importantly, precious time. The technology behind protecting sensitive and confidential information has also evolved with the help of methods like encryption and advanced authentication, giving customers confidence in the entire KYC process.

Know Your Customer process will help in making the customer understand that they are associated with a legitimate company.

With AML and KYC regulations, the organization can quickly identify whether the transaction executed or proposed to be executed with a particular customer is legal or illicit. The anti-money laundering KYC regulations include the authentication of customers, document verification like address proof, biometric verification, and face verification. It also requires identification and periodic updating of customer’s sensitive and personal information. When these steps are followed, noticing any unusual movement by any customer becomes relatively easier to notice.

Business enterprises usually start to recognize their clients with their general credentials. The client is then evaluated for authenticity. Customer due diligence or CDD aids the organization in this situation. It keeps the organization protected against the evils of money laundering and financing or terrorist activities from high-risk customers such as criminals, Politically Exposed Persons (PEPs), and terrorists posing a risk to the business organization.

This helps the business entity identify the category of due diligence to be applied to a specific customer, for example, enhanced due diligence (EDD) for customers who belong to high-risk categories. Lastly, regular monitoring of the customers is necessary as part of the KYC process.

What is KYC documents?

KYC documents include the documents that facilitate identity verification and address proof verification. ID cards and Utility bills are the most basic forms of KYC documents.

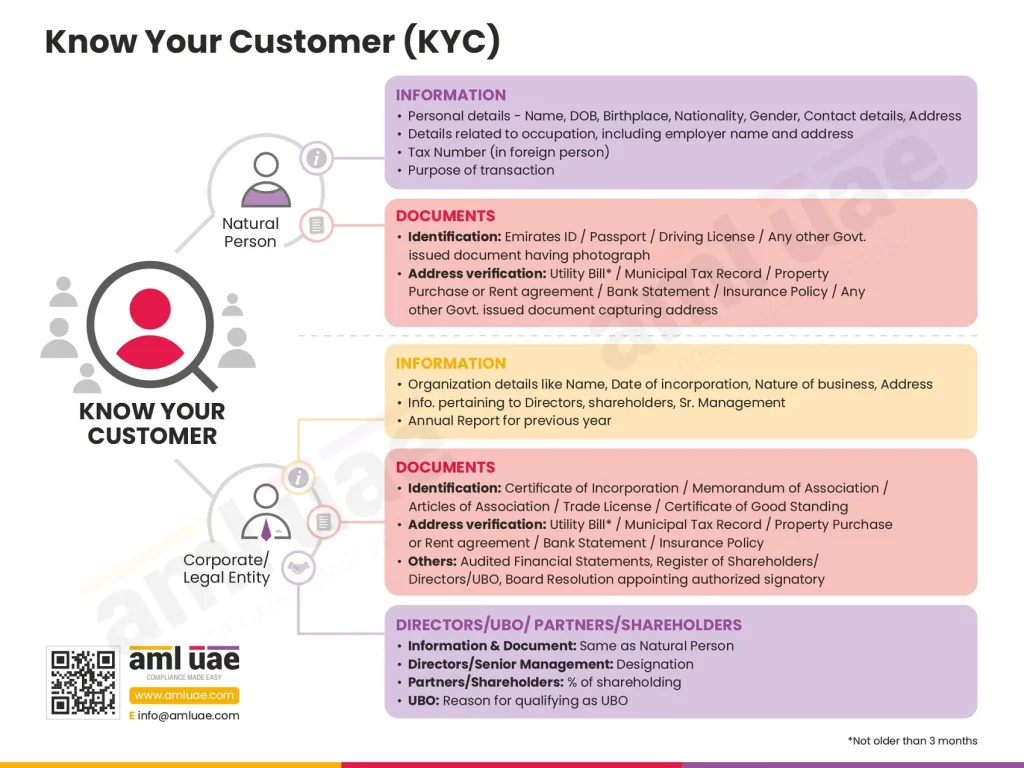

What are the KYC documents required for individual customers (natural persons) in UAE?

For individual customers (natural persons), the following KYC documents are required:

KYC Documents for an Individual Customer’s Identification:

Emirates ID/Passport/Driving License/Any other Government issued document having a photograph

KYC Documents for an individual Customer’s Address Verification:

Utility Bill (not older than 3 months)/Municipal Tax Record/Property Purchase or Rent Agreement/Bank Statement/Insurance Policy/Any other Government issued document capturing address

What are the KYC documents required for corporate customers (legal persons) in UAE?

For corporate customers (legal persons), the following KYC documents are required:

KYC Documents for a Corporate Customer’s Identification in UAE:

Trade License/Certificate of Incorporation/Memorandum of Association/Articles of Association/Certificate of Good Standing

KYC Documents for a Corporate Customer’s Address Verification:

Utility Bill (not older than 3 months)/Municipal Tax Record/Property Purchase or Rent Agreement/Bank Statement/Insurance Policy/Any other Government issued document capturing address

Other KYC Documents for a Corporate Customer’s Onboarding:

Audited Financial Statements, Register of Shareholders/Directors/UBOs, Board Resolution appointing authorized signatory

Implementing an effective KYC process

Step 1 - Customer profiling

Step 2 - Customer identification

Step 3- Transaction monitoring

Step 4- Risk management

Know Your Customer process under UAE AML Regulations

About AML UAE

AML UAE provides AML Consulting Services in UAE to help businesses remain compliant with the provisions of AML Law. AML UAE can help you implement an ideal KYC process in Dubai, UAE and train your staff in carrying out customer identification and verification. Get in Touch Now!

Our recent blogs

Share via :

Frequently Asked Questions (FAQs)

What is know your customer (KYC) as per Anti-Money Laundering Laws in UAE?

KYC, or Know Your Customer as per Anti-Money Laundering Laws in UAE is a process of identification and verification of your customers before initiating any business transactions with them.

What is involved in KYC checks?

As per the KYC regulations, KYC checks involve checking customers’ KYC documents such as identity proofs and address proofs to confirm their name, address, and other details.

Why is KYC important for companies?

Know Your Customer (KYC) is important for companies to confirm the identity of customers to help prevent cases of money laundering, identity thefts, or any other financial crimes.

What are KYC checks?

KYC checks include the procedures to explore and verify the identity of clients, customers, or suppliers to identify any potential risks of money laundering, illicit financial activities and identity thefts.

What is KYC process?

The KYC process under KYC regulation involves:

- Collecting information on your customers

- Validating information through KYC documents

- Verifying through checks

What are ‘know your customer’ requirements?

The ‘know your customer’ requirements include knowing and maintaining records on your customers’ identity and verifying these records through KYC documents to reduce the possibility of money laundering and other financial crime risks.

When does the KYC apply?

Here are a few situations or circumstances in which KYC is applied

- Buying precious metals and stones

- Incorporating a new company in UAE

- Opening a new deposit or borrowing account

- Opening a subsequent account where documents submitted as per existing Know Your Customer standards are insufficient while opening up the initial account.

- When the financial institution or DNFBP experiences the need to obtain additional information about the existing customer based on the customer’s conduct or sudden change in behavior

- When there are any kind of changes to signatories, beneficial owners, or mandate holders

What are the three components of knowing your customer?

Here are the three main components of knowing your customer (KYC)

- Customer Identification Program (CIP)

- Customer Due Diligence (CDD)

- Continuous/regular monitoring

What is Know Your Client (KYC)?

Know Your Client is a critical process for a Financial Institution, Designated Non-Financial Business and Profession, and Virtual Asset Service Provider to identify and verify its clients to assess and manage risks associated with them and comply with the Anti-Money Laundering Laws.

What are the steps involved in KYC process?

There are three steps involved in KYC process:

What KYC documents do I need to collect in UAE to comply with the AML Law?

KYC documents to collect in case of a Natural Person:

- Personal Data

- Passport/Emirates ID/Any other ID Card (Issued by Government) providing information as to name, nationality, date of birth and place of birth, and national identification number of a natural person

- Principal Address

- Bills or account statements from public utilities, including electricity, water, gas, or telephone line providers or;

- Local and national government-issued documents, including municipal tax records or;

- Registered property purchase, lease, or rental agreements or;

- Documents from supervised third-party financial institutions, such as bank statements, credit or debit card statements, or insurance policies.

KYC documents to collect in case of a Corporate:

- Personal Data

- Passport/Emirates ID/Any other ID Card (Issued by Government) providing information as to name, nationality, date of birth and place of birth, and national identification number of partners, directors, shareholders, and authorized signatories.

- Certificate of Incorporation, Trade License of the legal entity

- Principal Address

- Bills or account statements from public utilities, including electricity, water, gas, or telephone line providers or;

- Local and national government-issued documents, including municipal tax records or;

- Registered property purchase, lease, or rental agreements or;

- Documents from supervised third-party financial institutions, such as bank statements, credit or debit card statements, or insurance policies.

Add a comment

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is a Chartered Accountant with more than 25 years of experience in compliance management, Anti-Money Laundering, tax consultancy, risk management, accounting, system audits, IT consultancy, and digital marketing.

He has extensive knowledge of local and international Anti-Money Laundering rules and regulations. He helps companies with end-to-end AML compliance services, from understanding the AML business-specific risk to implementing the robust AML Compliance framework.