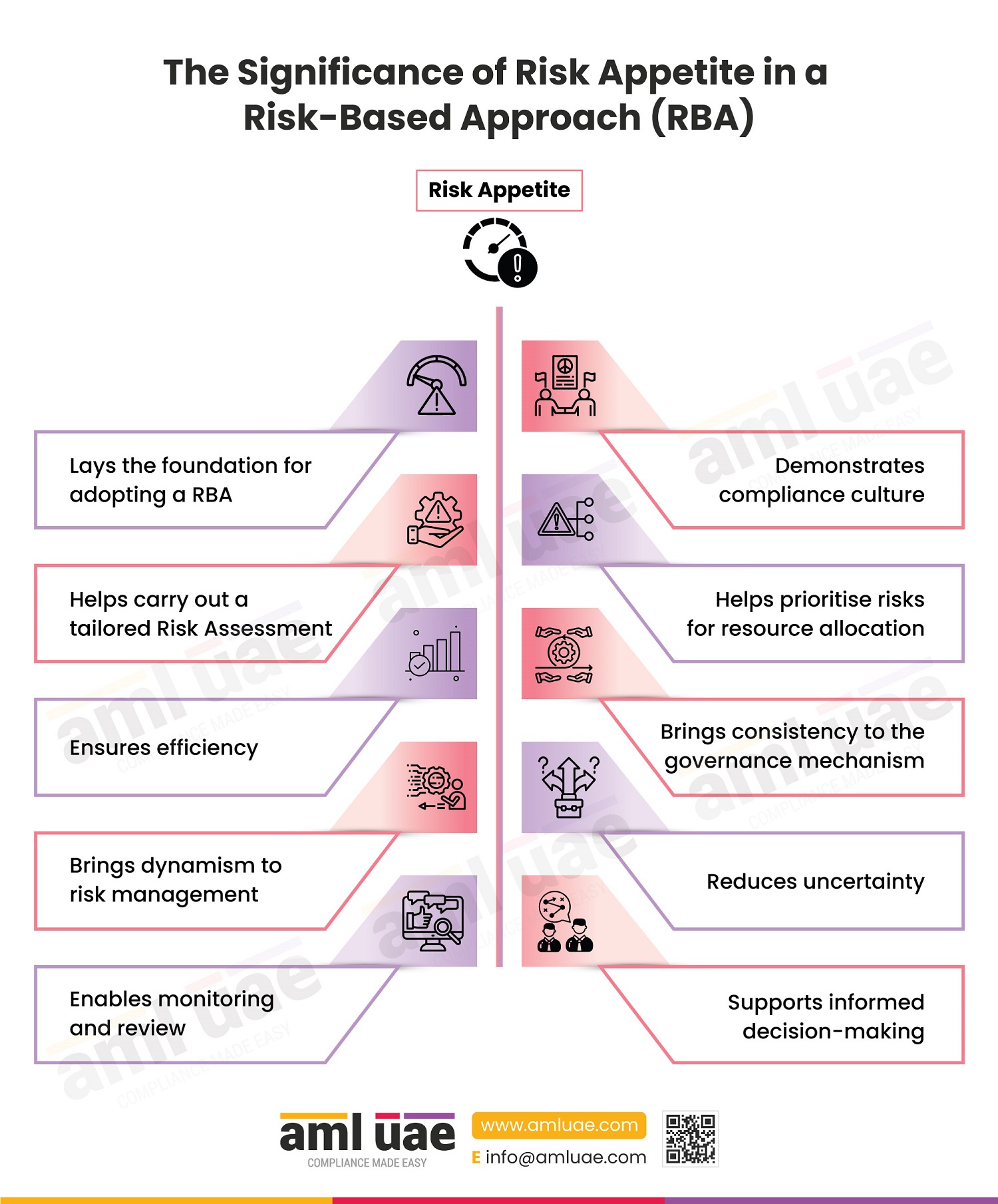

The entities must adopt the RBA and apply it uniformly across the company. Some entities fail to adopt it and deploy controls commensurate with the nature, size, and complexity of business, client relationships, geographies, delivery channels, and products and services.