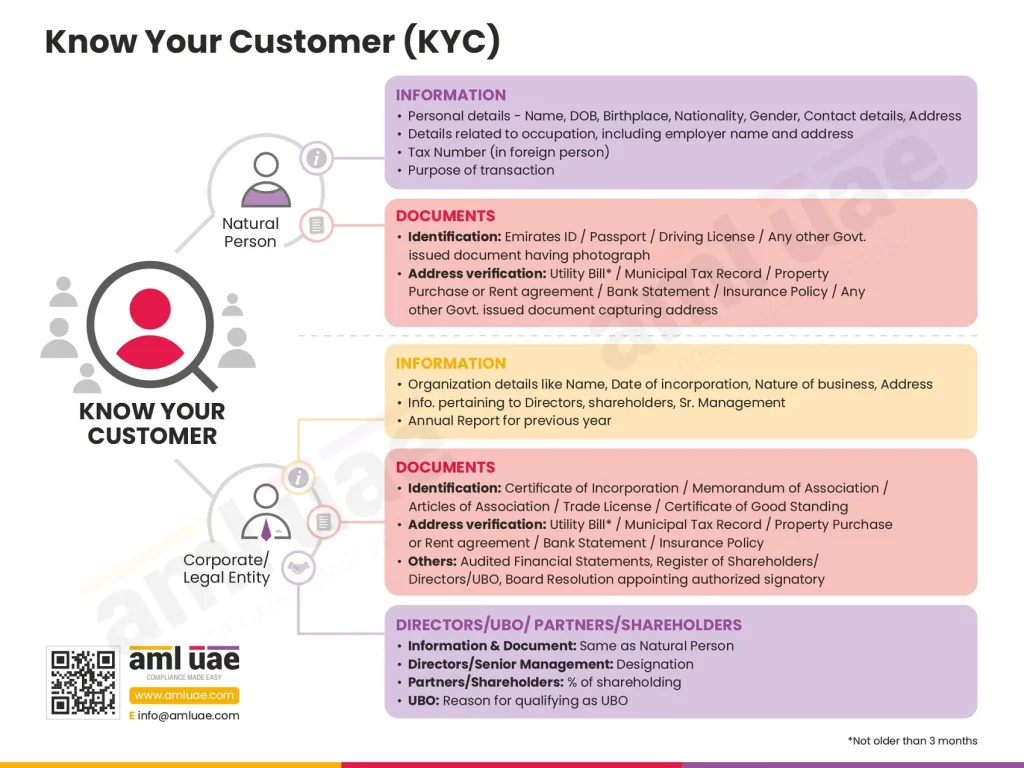

The basic requirements of KYC and CDD involve identification of the customer and their crucial information like nationality, contact details, address, business activities, the purpose of the transaction, etc., and verifying the authenticity of the information to determine the overall risk to the company from the particular customer, before onboarding the customer.