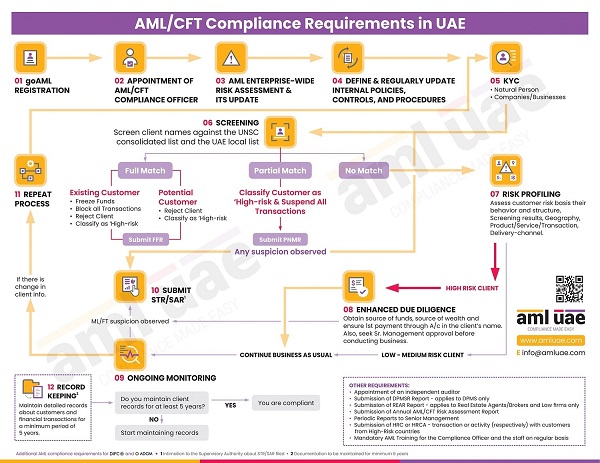

Anti-money laundering (AML) measures are crucial for every designated non-financial business and professionals (DNFBPs) operating in the UAE to safeguard their businesses against money laundering, terrorist financing, and proliferation financing. These measures are implemented throughout the customer lifecycle to ensure compliance with regulatory requirements and mitigate the risks.

Let’s understand the AML measures adopted at different stages of an individual (natural person) customer lifecycle: