A Guide to Establishing an Effective AML/CFT Framework in Your Business

Financial Institutions and Designated Non-Financial Businesses and Professions that do not abide by the Money-Laundering laws or regulations have to pay heavy penalties and face severe reputational losses. Therefore, every business has to establish an effective AML/CFT framework to operate as per the legal requirements of the country.

So, the question arises: what should you consider when managing AML/CFT compliance in your business? This article provides the best practices for establishing an effective AML/CFT framework in your business.

Compliance. Trust. Transparency

Customized and cost-effective AML compliance services to support your business always

What is an Anti-Money Laundering Framework?

Implementing elements of the Anti-money laundering (AML) framework using a risk-based approach is crucial for preventing money laundering, financing terrorism, and proliferation financing (ML/FT and PF). The AML framework is a set of policies, procedures and controls that are formed to detect, deter, and report ML/FT and PF activities.

The AML framework lays down a structured strategy that aims to fulfil regulatory obligations and achieve mitigation of ML/FT and PF risks.

Importance of an Anti-Money Laundering Framework

The following is a list of factors stating why the AML framework is essential:

Ensure regulatory compliance:

DNFBPs are required to comply with different AML regulations, including regulations imposed by national and international regulators. In case it fails to comply with such regulatory requirements, penalties and fees are imposed on DNFBPs. Therefore, with the implementation of an effective AML framework, they can ensure compliance with these regulations and stay away from associated penalties and fines.

Risk mitigation:

The major threat to DNFBPs is using their platforms to facilitate financial risks. Criminals often use them to indulge in criminal activities because of inherent vulnerabilities. The AML framework employs measures that help DNFBPs in detecting ML/FT and PF activities and further aid in combating ML/FT and PF risks.

Protect business’s reputation:

As DNFBPs work in a highly competitive market, it is essential for them to maintain a good reputation to attract and retain clients and customers. Commitment to AML compliance can act as a deciding factor for clients to enter into a business relationship with the DNFBP. Any linkage to ML/FT and PF activities can damage its reputation, which results in client and business loss. The AML framework helps DNFBPs avoid risk and maintain their reputation by laying down the best strategy within its framework.

Maintain the integrity of the financial system:

By promoting stability, preventing illicit activities, risk management, and regulatory compliance, the AML framework helps maintain the integrity of the financial system. With such measures, the AML framework enables a safe, secure and strong global economy.

Regulatory requirements around AML/CFT framework

AML regulatory framework in the UAE includes national regulations, international regulatory framework and national AML strategy.

National Regulatory Framework

The national regulatory structure in the UAE contains federal civil, commercial and criminal regulations. Because criminal legislation comes under federal jurisdiction throughout the country, the ML/FT and PF criminal activities are covered under it. The following are such regulations within the country:

- Federal Law No. 20 of 2018 on Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations.

- Cabinet Decision No. 10 of 2019 Concerning the Implementing Regulation of Federal Law No. 20 of 2018.

- Cabinet UBO Resolution No. 58 of 2020 on the Regulation of the Procedures of the Real Beneficiary (UBO Resolution)

International regulatory framework

The AML framework in the UAE is aligned with the international bodies network, which implements international treaties and conventions for combating illicit crimes. These integrated laws are supervised by the regional regulatory authorities.

For such an integrated framework, the government and competent authorities in the UAE collaborated with various international bodies such as:

- United Nations

- Financial Action Task Force (FATF)

- Middle East and North Africa Financial Action Task Force (MENAFATF)

- Egmont Group of Financial Intelligence Units

National AML Strategy

The UAE government has implemented strategic decisions in the form of the National Strategy on Anti-Money Laundering and Countering the Financing of Terrorism. The strategy shapes the key initiative of the country’s national action plan. This strategy is based on four pillars that include:

- Legislative & Regulatory Measures

- Transparent Analysis of Intelligence

- Domestic and International Cooperation & Coordination

- Compliance and Law Enforcement

Furthermore, the National Committee for Combating Money Laundering and the Financing of Terrorism and Illegal Organisations looks into the implementation of strategy, emphasising effective coordination between different authorities, compliance with regulations and awareness of ML/FT risks among DNFBPs.

Compliance. Trust. Transparency

Customized and cost-effective AML compliance services to support your business always

Regulatory Obligations and AML/CFT Framework

The AML framework needs to be aligned with the statutory obligations of DNFBPs as follows:

ML/FT Enterprise-Wide Risk Assessment

ML/FT Enterprise-Wide Risk Assessment, also known as Business Risk Assessment, is an assessment that lays down an extensive plan that needs to be carried out to manage ML/FT and PF risks at an enterprise level. EWRA is a key pillar of a risk-based approach that addresses business-specific AML risks, threats, and vulnerabilities and further takes action to mitigate them.

EWRA is a continuous process to identify and assess ML/FT and PF risks that DNFBPs face in business lines, their products, and services and associated with different customers. While conducting the assessment, it considers various internal and external factors such as geographical risks, customer behavior, distribution channels and adequacy of the current AML policies.

DNFBPs with EWRA can effectively detect money laundering risks, identify mitigating measures, point out gaps and take cautious decisions relating to risk appetite and allocation of resources.

Customer Due Diligence

Customer Due Diligence (CDD) is an extensive process to identify and verify customer identity with the help of verified documents. CDD process also includes assessing customer risk profile, understanding the nature of transactions and monitoring customer activities. Additionally, it also focuses on assessing risk associated with customer’s business relationships and transactions.

Further, the CDD process differs depending on the ML/FT and PF risks that customers are associated with. CDD comes in three types: Simplified Due Diligence, Standard Due Diligence and Enhanced Due Diligence. Different CDD types are employed for each customer to mitigate ML/FT and PF risks, depending on the circumstance.

Ongoing Monitoring

Only after CDD measures are employed for customers can DNFBPSs establish business relationships with them. Once they enter into these relationships, DNFBPS must undertake ongoing monitoring measures. This measure is crucial as it continuously detects and reports suspicious activities.

Further, as part of ongoing monitoring, DNFBPs monitor business relationships with each customer on an ongoing basis to prevent any probable ML/FT and PF activities which an existing customer can pose.

DNFBPs also need to undertake ongoing monitoring of transactions. In order to undertake such a measure, they need to implement a robust transaction monitoring system that can detect suspicious activity effectively by pointing out unusual patterns and frequent transactions and alerting the involvement of high-risk jurisdictions.

Regulatory Reporting

It is a regulatory obligation under the UAE’s AML regulatory framework to swiftly report suspicious transactions or any reasonable situation where any suspicion relating to proceeds is in question. DNFBPs in the UAE must put in place and update indicators that could be used to identify possible suspicious transactions.

Regulatory reporting means submitting various reports provided under the AML/CFT regulatory framework to the relevant authorities. In the UAE, Suspicious Activity Report (SAR) or Suspicious Transactions Report (STR) are standard reports filed by DNFBPs to report any suspicious activity they come across.

Furthermore, in addition to SAR/STR, they must also file reports depending on the circumstances and nature of their business. These include filing of Partial Name Match Report (PNMR), Fund Freeze Report (FFR), Real Estate Activity Report (REAR), Dealers in Precious Metals and Stones Report (DPMSR), High-Risk Country (HRC), and High-Risk Customer Activity (HRCA) reports.

AML/CFT Governance

For an effective AML framework, DNFBPs must include AML/CFT governance within their AML framework. This governance measure acts as a foundational structure. DNFBPs must include the following measures within AML/CFT governance:

- AML governance must include compliance staffing and training to ensure that compliance officers and employees understand their responsibilities surrounding AML and further effectively undertake them.

- It is mandated by the UAE’s regulatory framework that senior management is involved in the institution of the AML framework. Further, the law imposes various responsibilities on it, such as implementing governance and operating systems, approval of internal policies, procedures, and controls, application of the directives of Competent Authorities, and oversight of the AML/CFT compliance programme.

- The AML framework must include an AML/CFT health check mechanism within DNFBPs that evaluates the business’s performance against all applicable AML/CFT obligations. This measure establishes ways to oversee vulnerabilities across DNFBPs, thereby strengthening the effectiveness of AML policies.

- AML governance must include AML Independent Audit measures to evaluate efficacy and adherence to AML measures. It is an essential factor of the AML framework to engage auditors for conducting thorough reviews of current policies, procedures, and controls.

Record Keeping

Having a record-keeping system is essential within the AML framework. Records are an important source of information not only for DNFBPs but also for regulators. With record keeping, it is easier to undertake investigations and ensure transparency. As per the UAE’s AML regulatory framework, it is mandated that DNFBPs keep comprehensive information related to transactions, CDD, and any SAR/STR for five years.

Maintaining such records helps in identifying potential ML/FT and PF activities and underscores regulatory oversight. By keeping such records, DNFBPs can effectively counter ML/FT crimes and further safeguard themselves. Furthermore, having robust record-keeping practices, DNFBPs can effectively respond to regulators and commit to having a transparent and answerable culture.

Targeted Financial Sanctions

Targeted Financial Sanctions (TFS) include measures that the regulatory authority imposes to restrict financial transactions with specific individuals, entities, or countries. DNFBPs must undertake such measures to prevent transactions with sanctioned individuals or entities and freeze their assets when identified.

To avoid indulgence with ML/FT and PF risk, DNFBPs, as part of this measure, undertake screening procedures for customers against relevant sanctions lists released by national and international bodies and further report any matches to the appropriate authorities.

How to frame effective AML Controls framework?

Here are a few ways in which you can effectively build AML Controls Framework:

1-Having Qualified Compliance Professionals

The first and foremost step to building an effective AML and CFT framework is to have an effective and efficient AML expert who wouldn’t shy away from taking the help of creativity and innovation.

A practical AML/CFT framework requires a structure of corporate

governance that incorporates compliance professionals or officers who are fluent in terms of legal regulations requirements.

Anti-money laundering professionals are basically responsible for making sure that the reported issues within the organization are addressed or looked after within the organization and within a time frame that will restrict you from further damage.

In addition to that, it is your moral duty to make all the employees of your organization and not just AML professionals know about the legal and ethical responsibilities that need to be effectively managed at an individual level as well in order to comply with the legal AML regulations.

Furthermore, all the employees must understand the fundamental idea of AML/CFT. In order to effectively comply with AML or CFT regulations, all the employees must undergo interdisciplinary training or certification programs in order to identify potential risks.

2- Training of Anti-Money Laundering Experts

Anti-money laundering is a pretty dynamic subject. There is always some sort of updates, changes in regulations, proposals, or laws happening. In addition to that, various methods continue to find channels in criminals with every passing day.

Improving the overall skill set of your employees is essential in order to ensure that AML/CFT measures are actually implemented in the best possible way.

Professionals from the finance department must clearly understand the AML and CFT legislation and regulations for identifying and reporting any suspicious transactions.

Likewise, management employees who have direct contact with customers or the ones who process documents and money must understand the requirements of the Anti-Money Laundering Laws in the UAE.

Your entire staff must be well aware of the AML/CFT Framework and various roles of the consultants, compliance officers, officers, senior management, and the board of directors.

In addition to that, all of your staff members must be aware of ways in which they are supposed to react if at all they encounter suspicious activity.

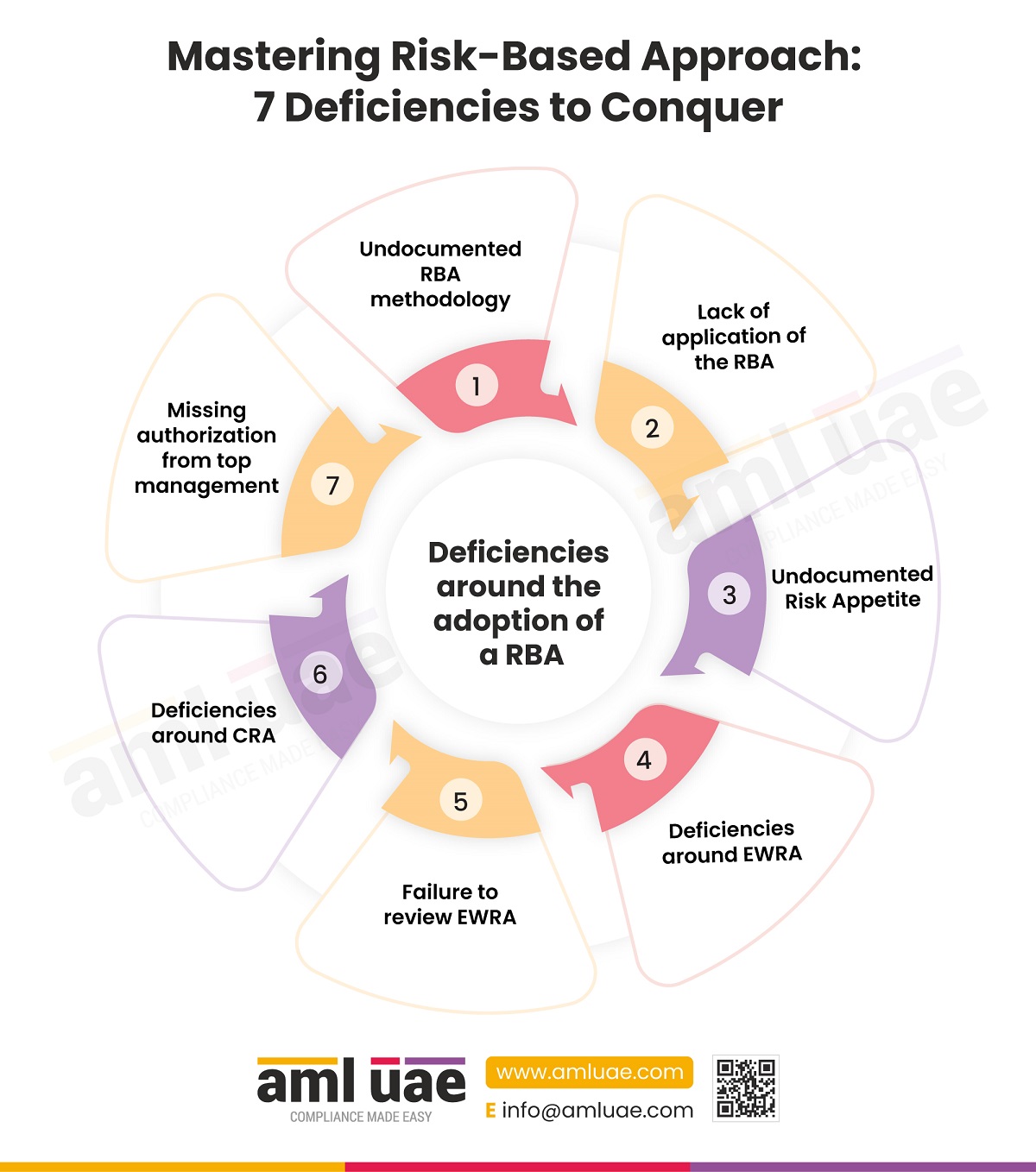

3- Risk Assessment And Risk-Based Approach

The foundation of a practical counter-terrorism financing framework (CFT) and anti-money laundering (AML) is actually based on a risk-based approach.

Business enterprises should determine the risk level of the clients by conducting an accurate risk assessment during the process of client

recruitment.

Post this, enterprises should aim to implement an efficient and effective AML compliance program in accordance with the AML/CFT Framework. By developing a tailor-made control program in accordance with the risk levels of your respective clients.

- Building policies and adequate controls to reduce the risk and even the potential of money laundering

- Understanding the overall levels of risks associated with business transactions and relationships

- Identifying various sources of risks and evaluating all the potential risk reduction controls

- Effectively running the successful AML compliance programs

- Making accurate risk-based decisions about the employees as well as customers.

In addition to that, a risk-based approach is adopted in order to detect and prevent all sorts of money laundering activities.

However, risk-bearing capacity and the risk appetite of all the companies and customers are pretty different from one another. As a result, companies would be failing miserably if they try to implement the same AML controls for every customer.

There are basically two fundamental steps for organizations to move ahead with a risk-based approach. The first one is undoubtedly assessing the risk and the second one is to appropriate control processes to various risk levels.

4- Advanced Anti-Money Laundering Policies

Highly dynamic anti-money laundering policies are needed to protect a business enterprise from criminal activities like money laundering and fully comply with relevant regulations and laws.

Enterprises need to implement robust risk-based governance to guide systems and processes. Providing a practical anti-money laundering policy framework is the topmost priority when it comes to meeting AML obligations.

Anti-money laundering policies should be easily verifiable by the authorized regulators, reflecting the overall risk appetite.

For instance, your AML policies should incorporate customer risk ranking during the recruitment process and due diligence.

Business enterprises should know their customers in order to comply with local and global legal anti-money laundering requirements and operate within the purview of the established AML/CFT Framework.

5- Know Your Customer (KYC)

Know your customer processes incorporate the process of accurately and completely defining the information of the respective customers. Generally, KYC is the most critical step in the entire anti-money laundering control process.

Once you are sure of who your customers really are, the risk levels of these customers can be evaluated without any hassle, and post which, you can apply customer due diligence (CDD) processes.

Determining the level of risks of your customers or even potential customers with the help of CDD makes the AML control process much faster and efficient for the company.

During the process of CDD, the potential customer must be screened in politically exposed persons (PEPs) and the sanction list.

If any politically exposed person is found in this list, then the need and importance of enhanced due diligence (EDD) come into the picture.

This is simply because politically exposed persons are usually considered as individuals who hail from a high-risk profile, and thus, merely CDD processes might not be sufficient. As a result, the risks and threats related to the customer’s account opening can be detected, allowing you to take more effective AML controls and establish a highly-effective AML/CFT Framework.

6- Ongoing Monitoring

Information or risks of institutions or customers may change over a period of time. For example, individuals who are not PEP might become politically exposed person by taking up any new task.

Hence, it is essential to be familiar with the information of the customer that may change over a period, also changing the risk levels of that particular customer.

Therefore, all of this information should be updated in your systems at regular intervals.

In addition to that, the accuracy of this information should also be confirmed so that it does not lose its functions of the risk-based approach.

If you are unable to keep up with the constantly changing customer information, you have to be prepared for some severe consequences.

The AML and CFT framework or policies makes an effective risk management tool. Additionally, an effective AML and CFT regime also reduces the probability of damage to the organization due to fraudulent activities.

7- Detecting And Reporting Any Suspicious Transactions

The primary purpose of anti-money laundering checks is to detect financial crimes and suspicious transactions. Financial crimes must be detected, and necessary precautions must be taken in order to bring your AML processes to their actual purpose.

Although it is pretty challenging to check suspicious transactions almost instantly, they can be detected with the help of transaction monitoring solutions available to you. All of these transactions are stopped immediately and passed onto some other AML experts.

8- Upgrade The Anti-Money Laundering System With AI-Powered Solutions

With the constant technological change, crimes are also changing their pace and ways dramatically, resulting in the evolution and development of the regulations. With this given, manual anti-money laundering controls remain insufficient in organizations that are prone to the risk of money laundering activities.

AI-powered anti-money laundering software solutions help you track the unusual transactions for the known patterns, and they reduce the risk of ML to a greater extent and thereby help in implementing an effective AML/CFT Framework.

Conclusion on Effective AML/CFT Framework in Your Business

The anti-money laundering (AML) framework is vital for preventing ML/FT and PF risks. Policies, procedures, and controls established under the AML framework help to detect, mitigate, and report illicit activities, including ML/FT and PF.

Additionally, as a structured strategy, the AML framework aids in a better understanding of the UAE’s AML/CFT regulatory compliance, thus ensuring compliance and avoiding penalties and fines. Therefore, with the implementation of the AML framework, DNFBPs can protect themselves from ML/FT and PF activities.

FAQs on Effective AML/CFT Framework

AML/CFT is essential for the following reasons.

- In order to protect the financial systems

- In order to prevent criminals or money launderers from enjoying the proceedings of the money laundering activities

- In order to restrict the criminals to develop formidable economic powers and challenge the stability.

If you are a financial institution or a designated non-financial business or profession, then the chances are pretty high that you are more prone to encounter pretty risky situations on a daily basis. Hence, each employee should be aware of the AML/CFT policies of your company so that they can also play their part effortlessly.

However, it will be the responsibility of the AML Compliance Officer to ensure that an effective AML/CFT Framework is implemented in the company.

Begin your AML compliance journey with a positive first step.

Contact our team to handle your goAML registration process.

Add a comment

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is a Chartered Accountant with more than 25 years of experience in compliance management, Anti-Money Laundering, tax consultancy, risk management, accounting, system audits, IT consultancy, and digital marketing.

He has extensive knowledge of local and international Anti-Money Laundering rules and regulations. He helps companies with end-to-end AML compliance services, from understanding the AML business-specific risk to implementing the robust AML Compliance framework.